The Investor's Blind SpotA Framework for Classifying Founder Charisma

Introduction

Last week I published a paper about five founders who blew up companies. Neumann, Watt, Holmes, Milton, Bankman-Fried . Over a hundred billion dollars evaporated. The inbox filled up. People asked two questions. First: how do I protect myself? Second: what about Jobs, Knight, Bezos? They were charismatic too. What's the difference? Although anyone who remembers Bezos in those late-nineties Amazon commercials might question whether 'charismatic' is the right word. Charisma, it turns out, is not fixed. It can be built. It can be performed. And it can be faked. That's the problem.

This paper answers both questions. It gives you a framework for telling the difference between charisma that builds companies and charisma that destroys them.

If you're a partner at a venture fund. If you're on an investment committee. If you allocate capital. If you sit on a board. If you evaluate founders for a buyout fund. This is for you.

1. The Framework: Builders vs. Performers

Every founder in this paper is charismatic. Jobs was charismatic. Neumann was charismatic. Holmes was charismatic. Charisma tells you nothing about whether the company is real. But it does tell you something about yourself. If you feel the pull, that electric certainty in the room, treat it as a signal. Not a signal about the founder. A signal about your own susceptibility. Every time. Whether the founder is genuine or not. You need a lens that works regardless.

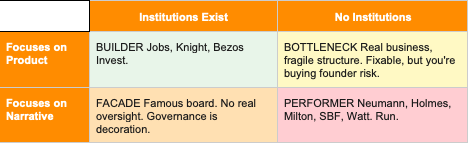

The framework has two dimensions. Two questions you can answer from observation.

Dimension 1: What does the founder focus on? The product or the narrative? Measure the ratio. How much of the founder's time, energy, and language goes into the product versus the story about the product? Jobs spent his days in design reviews, obsessing over circuit boards no one would see. That is focus on the product. Watt spent his days building a “punk” brand, picking fights with multinationals, and tweeting about revolution. BrewDog's marketing was world-class. Its governance was nonexistent. That is focus on the narrative. The ratio tells you what the founder actually cares about. Not what they say they care about. What they do.

Dimension 2: What has the founder built around themselves? Are there structures (a real board, real governance, people who can say no) that could survive the founder's departure? Or has the founder dismantled every check? Knight built Nike with a real board and real succession planning. Bezos stepped down and Amazon continued. Now look at the other side. Milton had no one reviewing his public statements before he made them. Bankman-Fried had no board to speak of. One builder, one absence of governance. The difference is visible from the outside.

These two dimensions give you four quadrants:

Three things make this framework useful. First, it's observable. You don't need psychology training. You need two questions: what does this founder focus on, and who can tell them no? Second, it works whether the founder is genuine or not. Every charismatic founder should trigger the same check. You measure the ratio. You look at the governance. You do it every time. Third, it gives you a tool. Not theory. A grid you can put on a whiteboard in the IC room.

2. The Four Quadrants

Builders: Product + Institutions

Jobs was brutal. Knight nearly went bankrupt. Bezos is obsessive. None of them were easy. But four things set them apart from the founders who destroyed companies.

First: the relationship to reality. When things didn't work, Jobs killed them. The Newton. The Cube. He didn't rebrand them. He didn't invent metrics to make them look successful. He buried them and moved on. That is a relationship with reality. Painful, but real.

Second: how they handled bad news. Knight nearly went bankrupt multiple times in Nike's early years. He told his investors. He told his bankers. He didn't move money around in secret or fake a video. He faced the problem and scrambled for solutions in the open.

Third: they built institutions that could survive them. Bezos built a fourteen-page memo culture, a leadership principles framework, and a management bench so deep that when he stepped away, Amazon didn't flinch. The company wasn't Bezos. The company was what Bezos built.

Fourth: they tolerated dissent. Jony Ive pushed back on Jobs. Tim Cook pushed back on Jobs. The best people stayed at Apple because the argument was about the work, not about loyalty. You can build a great company around a difficult founder. You cannot build one around a founder who treats disagreement as betrayal.

Performers: Narrative + No Institutions

Adam Neumann gave himself supervoting shares. His vote counted for twenty ordinary votes. No independent chair. No governance structure that could override him. Meanwhile the narrative kept shifting: subleasing company to community company to consciousness company. Every time reality closed in, the story got bigger. When WeWork collapsed, Neumann walked away with one point seven billion dollars. SoftBank bought out his shares and extended him a credit line on the way out the door.

Elizabeth Holmes built Theranos around blood tests her machines couldn't perform. When the tests failed, she hid the results. When employees raised concerns, she fired them. She controlled the story so completely that investors went through multiple funding rounds without ever independently verifying the core technology.

Trevor Milton published a video of the Nikola One apparently driving under its own power. The truck had been towed to the top of a hill and rolled down with the brakes released. The camera was tilted to make the road look flat. The door was taped shut. He was convicted of securities fraud and wire fraud. In March 2025, President Trump pardoned him. The month before, Nikola filed for bankruptcy. Milton then tried to buy it back.

Sam Bankman-Fried ran FTX without an organisational structure at all. No risk committee. No compliance function. No org chart. When he moved eight billion dollars of customer funds into his trading firm Alameda Research, there was no one whose job it was to notice. The entire company was designed so that one person controlled everything and no one could say stop.

James Watt ran BrewDog without a chairperson for its entire history until the scandals forced one. Over two hundred and twenty thousand small investors bought into his 'Equity for Punks' crowdfunding. They didn't feel like investors. They felt like members of a movement. The identity replaced the analysis.

Five founders. Five different styles. One pattern: every one of them focused on the story, not the product. And every one of them made sure no one had the authority to say stop.

Facades: Narrative + Decorative Governance

This quadrant is rare but dangerous. The governance exists on paper. The board has famous names. But the names are there for credibility, not scrutiny. Theranos had Henry Kissinger, George Shultz, James Mattis, Sam Nunn, and William Perry on the board. Statesmen and soldiers, not scientists. They assumed that if people of their stature were involved, the company must be legitimate. That assumption was itself a comfort ritual. The governance was real in form and empty in function. If the board can't evaluate the product, the board is decoration.

Bottlenecks: Product + No Institutions

This is the founder with a real business and real talent but no structure around them. The product works. Customers are real. Revenue is real. But remove the founder and there's nothing underneath. This is fixable. You can build governance into a real business. But know what you're buying. If the founder gets hit by a bus, you own a shell. If you buy this, you need to put in structure, like as soon as they cash your equity check.

3. What to Look For in the Room

The framework is simple. Applying it is not. Performers are good at performing. Here are observable signals.

Red Flags: You're Probably Looking at a Performer

The metrics keep changing. Neumann introduced 'community adjusted EBITDA', a made-up metric that stripped out real costs to make losses look like growth. When the standard numbers don't support the story, Performers invent new numbers. If the KPIs shift every quarter to keep the narrative alive, the narrative is the product.

The founder has weakened or removed governance. Look at the cap table. Look at the board composition. Look at how strong the CFO is. If the founder has consolidated voting control, handpicked the board, or eliminated the independent chair, the checks are gone. Ask yourself: can anyone in this building tell the founder no and survive?

Dissent is punished. Watt's employees described a culture of fear at BrewDog. Milton told senior executives who raised concerns that they 'didn't understand capital markets.' When questioning the founder is treated as disloyalty, you are not looking at a Builder. You are looking at someone who has made the story unfalsifiable.

You can't explain what the company does. Neumann's famous pitch was twelve minutes long. Twelve minutes about reshaping how humans work. Not one minute about lease economics. If you leave the room feeling inspired but you can't describe the business model on a napkin, you've been performed at.

The persona is more developed than the product. Holmes had the turtleneck and the carefully lowered voice. Both were manufactured. Bankman-Fried had the cargo shorts and the beanbag. Watt had the punk rebellion and liked to wear tweed flat-caps. Milton was the blue-collar visionary in cowboy boots. When the personal brand is polished and the product is vague, the personal brand is the product.

Green Flags: You're Probably Looking at a Builder

The founder's time goes into the product, not the story. When Bezos's team proposed ideas, he interrogated the customer impact. Not the press release. Not the narrative. The product. If a founder spends more time on the thing itself than on how the thing is perceived, that's a signal.

The founder can describe failure without rewriting it as a triumph. Jobs was fired from Apple and spent years in the wilderness before coming back. He didn't pretend the exile was strategic. Knight's early letters to investors read like a man on the edge of bankruptcy. Because he was. If the founder's story has no setbacks, it's not a story. It's a pitch.

Strong people stay and push back. Talk to the senior team. Not the founder's favourites. The ones who've been there longest. Are they allowed to disagree? Do they? If the management bench is full of people who agree with the founder on everything, the founder has hired for comfort.

The product can be independently verified. Not in a demo they control. Not in a video they produced. When your own team tests it. When an independent engineer tests it. When no one from the company is in the room. If you can't verify the core product independently, you are buying the story, not the business.

4. Why You Fall For It

You know the framework. You know the red flags. You'll still fall for Performers. Here's why.

Groups push their anxiety into leaders. When your investment committee sits across from a charismatic founder, the group's collective uncertainty gets absorbed by the founder. The founder says: I know what to do. The group feels better. The group doesn't realise it's outsourced its thinking.

This isn't a metaphor. It's how groups work. Bion, a psychoanalyst who studied groups at the Tavistock Clinic after World War II, found that every group swings between rational mode and fantasy mode. In rational mode, the group thinks, analyses, and plans. In fantasy mode, the group looks for someone to save them. The investment committee thinks it's always in rational mode. It isn't.

The founder who eliminates your anxiety feels like a genius. The founder who makes you more anxious feels like a bad bet. But a Builder makes you think harder. A Performer makes you feel better. The feeling of certainty in the room is not data. It's a warning.

Not everyone falls for the same thing. Some people are wired to believe in the leader. Some are wired to fight or flee. Some are wired for hope, the belief that THIS founder will be the one. The wiring is personal, shaped by temperament and career. The venture capital industry selects for people wired to believe. That's the job. But being wired to believe doesn't feel like susceptibility. It feels like vision.

Sequoia invested in FTX. Sequoia is not stupid. But when Bankman-Fried walked into the room and talked about effective altruism, something in Sequoia said yes. Sequoia's wiring was talking louder than Sequoia's analysis.

What this means: Your conviction is not reliable data. Your attraction to a founder is information about you, not about the founder. You need people in the room who are wired differently. Who are not attracted to the founder. Let them talk. Don't dismiss them as cynical. They're not cynical. They're differently susceptible.

5. The Toolkit

The framework tells you what to look for. These interventions create friction in the moment. Use them together. Every time.

1. Separate the Founder from the Decision

Don't meet the founder Tuesday and decide Wednesday. Real separation. A week minimum. No informal discussion. The inflation effect is powerful in the moment and weaker over time. Give it time to weaken.

2. Ban the Pitch Deck. Require a Written Memo.

A slide with a hockey stick graph hides anything. A memo forces clarity. Require the founder to write down exactly what they're doing, why, and what the risks are. When Holmes had to explain her technology in writing, it fell apart. But she never had to. She pitched visually.

3. Appoint a Formal Devil's Advocate

Before every vote, one person presents the case for rejection. Not concerns. The case for no. This is a formal role. It creates space for dissent. Without it, the group protects its fantasy.

4. Apply the Framework Explicitly

Put the 2x2 on the whiteboard. Before every investment decision, the committee answers two questions together: what does this founder focus on, and who can tell them no? Plot the founder on the grid. Out loud. On the record. This forces the discussion.

5. Run the Founder Removal Test

Tell yourself: the founder will be removed in six months. For any reason. Would you still want this investment? If the answer is no, you're not buying a company. You're buying a feeling.

6. Track Your Body, Not Your Brain

After a founder meeting, write down what your body did. Not what you thought. Did your breathing change? Did you lean forward? Did you laugh at things that weren't funny? Your body is more accurate than your opinion. Your opinion is infected by the inflation. Your body is data.

7. Audit Your Conviction History

Go back through your investments. Find the ones where you had the highest conviction. Calculate the failure rate. The investments you were sure about have roughly the same failure rate as the investments you were cautious about. Your certainty is not skill. It's feeling.

6. Why Due Diligence Won't Save You

You do due diligence. You call customers. You check references. You spend weeks. Then the company collapses. How did diligence miss this?

It didn't miss anything. Due diligence isn't designed to find anything. Due diligence is a comfort ritual. Each item on the checklist gives you a moment of relief. You checked it off. You're allowed to invest. But due diligence is not designed to say no. It's designed to say yes with ritual.

SoftBank's analysts found that WeWork's unit economics didn't work. They documented the losses. They flagged the risks. Then SoftBank invested eighteen billion dollars. The diligence was thorough. The diligence said yes anyway. Because diligence isn't analysis. It's ritual.

Here's the test. In your fund's history, how many times did due diligence change a yes to a no? Count them. The number is smaller than you'd like to admit.

What this means: Use diligence. Do it carefully. But know what it is. It will give you permission to do what you've already decided to do. The checklist is a way of managing your anxiety. It will not prevent the next catastrophe.

7. The Edge

You have a framework. You have red flags and green flags. You have a toolkit. You have diligence. The next catastrophe will still happen.

What changes is this: you will see the dynamic while it's happening. You will tell your committee: this founder's time goes into the narrative, not the product. No one in the building can tell them no. We are looking at a Performer.

Naming it creates friction. Not between you and the founder. Between you and your own psychology. That friction is small. But it creates a gap. In that gap, something like analysis becomes possible.

You might still invest. You might still lose. But you'll invest knowing what you're doing. You'll see yourself in the system.

This is not a strategy. It's an edge. An edge is all that's available.

This framework is built on a field called systems psychodynamics. Eighty years of research into how groups actually behave under pressure. I have written a full explanation of the theory, the history, and the academic literature behind every idea in this paper. It is available at portobelloadvisory.com/blindspot. I won't pretend you're going to read it. Most finance types would rather chew glass. But it's there. And if you ever find yourself at a dinner party next to a psychoanalyst and need to hold your own for ten minutes, it's worth the click.

Sources and References

Bion, W. R. (1961). Experiences in Groups and Other Papers. Routledge.

Bion, W. R. (1962). Learning from Experience. Heinemann.

Klein, M. (1946). 'Notes on Some Schizoid Mechanisms.' International Journal of Psycho-Analysis, 27, 99-110.

Menzies Lyth, I. (1959). 'The Functioning of Social Systems as a Defence Against Anxiety.' Human Relations, 13, 95-121.

Rice, A. K. (1963). The Enterprise and Its Environment. Tavistock Publications.

Fraher, A. L. (2004). A History of Group Study and Psychodynamic Organizations. Free Association Books.

Shapiro, E. & Carr, A. (1991). Lost in Familiar Places. Yale University Press.

Kets de Vries, M. (1984). The Irrational Executive. International Universities Press.

Armstrong, D. (2005). Organisation in the Mind. Tavistock Institute.